Do Your Investments Match Your Values? Meet ESG Funds

There has been a growing movement among investors, to invest in companies that align with their morals and ethics.

There has been a growing movement among investors, to put their money where their mouth is by investing in companies that align with their morals and ethics. In this case, people who are interested in seeing responsible change around the areas of the (E) environment, (S) social justice and (G) governance, have started to buy “ESG funds”. The goal of these mutual funds is to buy into a set of companies that score well in these areas, while refusing to invest in companies that rank poorly. The basic notion - I am interested in being diversified across a set of companies, I want to have something that is managed, and I am interested in financially supporting companies that are aligned with my thinking.

Are you putting your money where your mouth is?

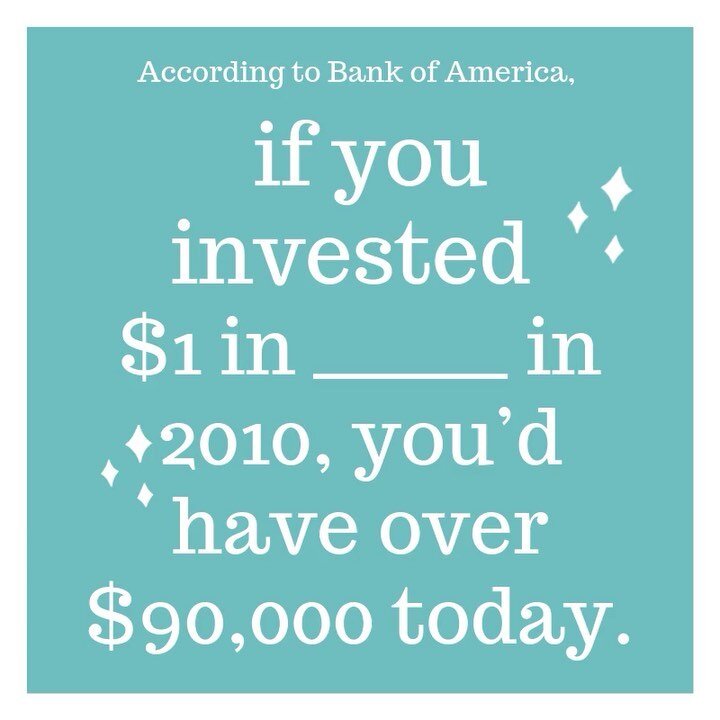

Did you know that buying a standard SP500 index fund, is putting money into cigarette makers, companies who hire child labor in foreign countries and gun makers?

To reach this objective, companies are scored based on how they measure up. MSCI is one company that provides a fairly standard measure. A mutual fund company will then invest in a set of companies that meet some criteria related to those measures. As an example, SUSL, a iShares ETF, only invests in companies that rate higher than “BB” in the MSCI ESG ratings. And expressly excludes companies deemed to be involved in problematic areas such as tobacco, alcohol, gambling, etc.

An interesting thing to note about many of these funds, is that they actually tend to perform as well as, if not better than the standard index/funds that invest in problematic companies.

You might think that it would be more costly to invest in these sort of funds. However, with a little research, you can find both super effective and inexpensive ETFs that meet ESG objectives, that actually have low expense ratios. Eg, SUSL, mentioned above, as a .10% expense ratio.

Yes!!! Investing in ESG funds can actually lead to better performance and be relatively inexpensive.

If you are interested in learning more about aligning your investing with your values, let’s schedule some time. ESG funds may be a perfect way to you to put your money where you mouth is.

Can You Fill A School With Artwork?

Besharat Gallery created a program to give away a large set of beautiful images, framed and installed, to elementary schools.

I was reminded of the benefits of a life well lived, while walking through Charlie’s school last week. The walls are covered by Steve McCurry’s art. You may not immediately recognize that name, but you definitely know his iconic artwork. This project was conceived and implemented by a friend, Massoud Besharat. Massoud strongly believes that kids need to be exposed early and often to art. Given the limited amount of time many school systems set aside for art, Massoud created a program to give away a large set of beautiful images, framed and installed, to elementary schools. Every day, the kids are exposed to this art as they walk around the halls. If you have not seen it, you really should walk through Talley St Upper Elementary as soon as possible.

A life well lived, is a beautiful and inspiring thing. Have you reached the point where you can easily give away a substantial gift, with the intent of helping many? And even better, right in your community?

With planning, sacrifice and heart, you too can reach this goal. Are you prepared to take the steps? How do you switch perspectives from accumulating to giving? How long will it take to accumulate this much? Who needs your help?

Lets set up some time to talk about how you can reach this goal.

Is the First Week In December the Ideal Couples Getaway Time?

I have friends who are jetting out of Decatur and heading to the beach. The first week of December.

Jenn and I have friends who are jetting out of Decatur and heading to the beach. The first week of December. I mean the family just left a few days ago from Thanksgiving celebrations., right? The house is finally cleaned after the melee. The holiday decorations are out, the tree is in the stand, the Elf on the shelf rules the mornings.

There are receipts to collect from day care and doctors offices. There are last minute projects at the house/office that need to be completed before the end of the year. The car needs to be serviced and needs new tires. Leaves!! So much raking needs to be done.

And they are going to the beach …

Brilliant!! I am glad to be surrounded by friends smarter than I.

Let me count the ways this actually makes sense:

The grandparents are in town, they can watch the kids

Thanksgiving can be stressful, its time for a quick pressure release

Christmas is right around the corner and can be stressful

It just turned cold, and a bit of sun and warmth is a good reminder of fun times to come

It is a good forcing function to get some family chores done

It has been a long year, and we have not had as much couples time as planned

It is a great time to evaluate the year

It is a great time to plan out the coming month

Everybody else just completed their travel, so it is not crowded or super expensive

The best books of the year lists are out … now you have some time to read one

This type of trip did not get factored into our yearly vacation budget. And next year’s is going to be pretty depleted after trips to New Orleans for Mardi Gras and Kenya in the summer.

But maybe Jenn and I need to discuss this for next year … what do we need to sacrifice to make this happen?

If only we had a few days at the beach to discuss at our leisure…

Are You Burned Out At Work? Take the Assessment

Most of us have to work. There are bills to pay. Kids to feed. Places to see. Food and wine to enjoy. Healthcare. Sometimes it’s because we love it (prior to starting my own financial advisory business, I believed this was mostly platitudes). Sometimes it can burn us out. A recent survey by millennials, found that work and finances were the 2 highest sources of burnout.

Do you wonder if its worth it? Is your job killing you a little bit every day? Are you feeling burned out?

A little of my own story

When I graduated from GA Tech, I already had a job. I worked at GE my final quarter of college, driving through traffic up to Windward Parkway during the week, learning about Cisco routers. And cramming in my final two courses in the hours between work. I then proceeded to work my tail off for the next 20 years, never really taking a major break. My tech career required that I always be plugged in. I worked with people in India, Israel, France, West coast … when I woke up in the morning, my inbox was filled. When I went to bed, if I was lucky, I had mostly cleared out the 400 emails that I received daily. Vacation was just another way of saying that I was working remotely from a desk with a cool view. By my early forties, I was making “good” money and making a difference at work, but I was feeling bogged down. A general feeling of malaise, that even fun travel destinations, could not shake.

I ended up taking a year off, to reevaluate and regroup. And came out of it in a much better situation.

What is burnout? Mental or physical exhaustion. There are 5 stages …

How do you know if you are entering that burn out stage? Are you currently burned out? Here are some things to look out for:

Are you constantly tired?

Are you not sleeping well?

Is your productivity slipping?

Are people you used to like at work, constantly irritating you?

Do you feel like you are constantly “on” and never get any time away?

Do you have a list of the 5 things you would prefer to be doing?

Do you dream about work and wake up in a cold sweat?

Are you self sabotaging?

Find yourself fantasizing about getting fired?

It is not an easy problem to solve. As is generally true, half the battle is realizing the situation. Are you talking to anyone about it? Are you mapping out a strategy to solve the problem?

Several things to consider:

Talk to your boss about it

Find a mentor and talk to them about it

Take a long vacation and completely unplug

Find a safe place to dream about what you really (realistically?) want to do

If finances cause you stress, wrap your arms around the problem. Is it debt? Keeping up with the Jones’? Expectations?

Buckle down and save 6 months worth of expenses. Then take a long break. Sometimes removing yourself from the situation will allow you to see more clearly.

Detach yourself from work. Set aside time during the day that you don’t check your email or Slack.

Make room in your day to meditate, work out, nap, play guitar … Rest is one of my favorite books on the topic.

Go easy on yourself

If you are feeling burned out, there are many ways to make forward progress. Know, that you only have one life, and it is up to you to solve the problem. Finances are a means to an end … your money is there to help you reach your goals. If you stash a huge pile of gold, it won’t add up to much if you are not using it for the things that make you happy.

7 Tips for Last-Minute Year-End Financial Planning

Thanksgiving is over. The turkey leftovers have all been used. The family has returned to their distant homes. And you have exhausted your Black Friday and Cyber Monday budgets. Now is the time to take a breath and make sure that your family is going to finish out 2019 strong. Are you ready to get started?

REVIEW YOUR OPEN ENROLLMENT OPTIONS AND OPTIMIZE YOUR SELECTIONS

Make sure that you and your spouse are coordinated on health care and dependent spending and 401k and Roth saving goals.

ADJUST YOUR TAX WITHHOLDINGS

If you have had a child in 2018, been through a divorce, changed jobs or had a change in income, you will likely need to adjust your withholdings.

FUND LONG TERM SAVINGS VEHICLES (401K, ROTH IRA, IRA, SEP IRA, 529S).

Contribution limits for your 401k increased to $19,000 and IRA is $6,000. Beware that there are limits on IRAs depending on your income. Remember that 401k and IRA contributions go in before taxes, which can increase the amount your money grows over time. Your Roth IRA contributions go in after taxes, which means you never have to worry about taxes in the future. If you are self employed, take the time to fund a SEP IRA, which has much higher limits than a standard IRA or 401k.

CHECK YOUR HEALTH AND DEPENDENT CARE FLEXIBLE SPENDING PLANS

Track down your receipts and enter them now. I like to use this wind fall to fund Christmas. If you have not used all of your money, its time to do it now. You still have some time to get in all the spending, but these are “use it or lose it accounts.” Also, if you have hit your health care deductible, it may make sense to hit the doctor one more time to take care of anything you have been putting off.

SET AN END OF YEAR BUDGET.

There is a lot going on: gifts, travel, family events, parties, family pictures. Start to think, at the very least, about some guard rails that you want to set. This is the time of the year that most Americans put on the majority of their weight … and incur the majority of their debt. Make this year different. You will feel great come January, when you wont have to create crazy goals to overcome the splurges.

START PLANNING FOR NEXT YEAR

Set up a meeting with your financial planner. Now is the time to start setting some longer term goals for next year and help secure your retirement for tomorrow. Let me guide you through the process and monitor your progress.

FOLLOW US ON INSTAGRAM: CHAMBERLAINFINANCIAL

How to Save $750 in Open Enrollment

Open enrollment is the time to maximize your coverage and 401k choices while minimizing your spend. Learn how to make the most of this opportunity.

It’s time. You’ve received your company’s annual mailers and email reminders, announcing that open enrollment is coming up. BE READY!! Let the fun begin! And how about those 25 page, thick paper, glossy photo brochures for your options? Everyone always looks so happy.

Calling all CDC, Cisco, Coke, Delta, Eaton, Georgia Pacific, Home Depot, Mailchimp, Siemens, State Farm and other GA professionals and families!! LISTEN UP.

The Goal

The goal of open enrollment is to update and optimize your elections, given any potential changes in your situation. What kind of changes?

Someone in the family is going to need braces or extra dental care?

You are planning to have a baby

Your significant other changed jobs

You got a raise and need to increase how much you put into your 401k

You are afraid that Trumps’s tariffs are going to bomb the market, and you need to reallocate your 401k

You never really thought about needing disability insurance, until now

Your kids are starting day care or aftercare and you heard you could invest pretax cash in a dependent care FSA

There are any number of things that could need to be updated. But most people mistakenly think this is just a boring chore, with little added value. And anyway, you made the elections last year, why spend the mental space on it again?

Or worse than complete ambivalence about the topic, you know you need to make some changes, but you are “too busy” to read the literature, preventing you from making a wise decision.

It is easy to end up spending an extra $750/year, with poor choices.

Focus on your vocation and vacation!

Schedule time with me to run through the options. THIS IS A GREAT OPPORTUNITY TO GET AN EASY WIN. I can point out how to maximize your coverage and 401k choices while minimizing your spend … all while focusing on your long term goals. We can get started looking over your options, over a cup of coffee, and it won’t cost you anything.

I’m looking forward to catching up with you.

**After publishing this blog, an interesting article was published from Kaiser Family Foundation data, showing that employee based healthcare costs around $20,000/year ($14k = employer, $5500 = employee)

Follow Us On Instagram: ChamberlainFinancial

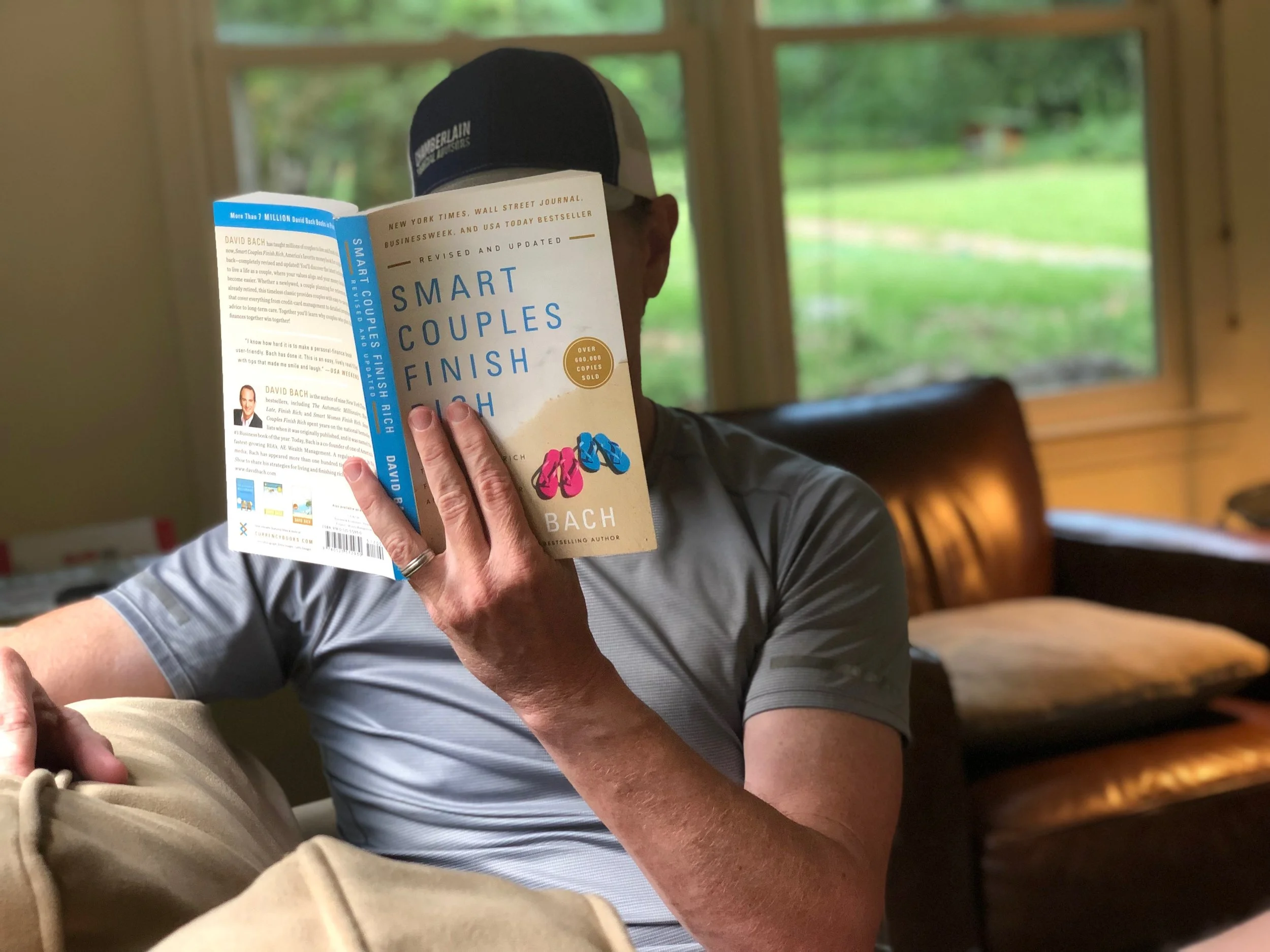

Take the "Smart Couples Finish Rich" Financial Knowledge Quiz

Take this financial quiz to see how you and your partner are doing with your finances.

When it comes to finances, David Bach and I have a similar outlook which includes that there is generally one CFO in a couple. However, just because there is a single CFO, both partners still need to understand and agree on the overall family finances. In our family, I’m the CFO, but together Jenn and I have established our goals and she knows how to access all of our investment and insurance accounts, if needed.

Given that it is very likely that you have one CFO, it is extremely important to understand what you both should “know” and what should “be able to get your hands on give an hour or so”. Take this quiz with your partner and check for your scores at the bottom. Reproduced from David Bach’s New York Times Best Seller, Smart Couples Finish Rich.

True | False I know our current net worth (i.e. the values of the assets we have minus the liabilities we owe.)

True | False I have a solid grasp of what our fixed monthly overhead is, including property taxes and all forms of insurance.

True | False I know how my partner feels about our monthly overhead. We have discussed both the size and nature of our regular expenses and obligations, and are comfortable with them.

True | False I know how much life insurance my partner and I carry. I know exactly what the death benefits are, how much cash value there is in our policies (if any), and what rate the money is earning (if applicable).

True | False I have reviewed our life insurance polices sometime in the last 12 to 24 months, and I am comfortable that we are paying a competitive rate in today’s insurance market.

True | False I know the current value of our home, the size of our mortgage, the interest rate on the mortgage, and how much equity we have in our home. I also know the length of our mortgage-payment schedule and how much it would cost per month to pay down the mortgage in half the time.

True | False I know what type of homeowner’s or renter’s insurance we have and what the deductibles are. I know whether or not our policy would provide us with ‘today’s replacement cost’ or actual cash value, if our home and/or property were destroyed or stolen.

True | False I know the nature and size of all our investments (including cash, checking accounts, savings accounts, money-market accounts, CD’s, treasury bills, savings bonds, mutual funds, annuities, stocks and bonds, real estate investments, and collectibles such as stamps, coins, artwork, etc) I also know where all the relevant paperwork is kept.

True | False I know the annualized returns of all the above-mentioned investments.

True | False I know the current value of all our retirement accounts (including 401(k) plans, 403(b) plans, IRA’s, Roth IRA’s, SEP-IRA’s, Keogh plans, company pension plans, etc.) I know where the statements for these accounts are kept and I have a solid grasp of how all our accounts performed last year.

True | False I know what percentage of our income we are savings as a couple.

True | False I know how much each of us is putting into our respective retirement accounts, whether that amounts to the maximum allowable contributions, and what our respective vesting schedules are.

True | False I know how much money each of us will be getting from Social Security when we retire, and what our pension benefits (if any) will be.

True | False I know whether or not we have a will or living trust, what its provisions are, and how up-to-date it is.

True | False I know whether our income would be protected by disability insurance should I or my partner become unable to work. If we do have disability insurance, I know the amount of coverage, when the benefits would start, and whether they would be taxable. If we don’t have disability insurance, I know why we don’t have it.

True | False I know what my partner’s wishes are regarding medical treatment (including being kept alive by artificial means) in the event he or she falls seriously ill or is seriously injured. I know whether or not our will includes a valid power of attorney covering such situations. I also know how my partner feels about being an organ donor.

True | False I know if my partner has taken an investment class in recent years.

True | False I know how my partner’s parents handled their finances and I know what effect that has had on how my partner feels about how we manage our money.

Scoring

Give yourself 1 point for every time you answered “True,” and 0 for every time you answered “False.”

14-18 points. Excellent! If you are the CFO, well you are doing your job!! Kudos. If you are the “not so much CFO”, you and your partner obviously have been planning together, as a result of which you have a good grasp of the state of your finances and how you both feel about money.

9-13 points. If you are the CFO, you have some work to do, you have some gaps in your responsibility. If you are the “not so much CFO”, you need to at least be aware of how you can answer these questions, in about an hour. Preferably by something provided by the CFO on some regular cadence.

Under 9 points. You and your partner don’t make a habit of talking about money, do you? As a result, your chances of being hurt financially because of insufficient knowledge are enormous . You need to learn how to work together in order to protect yourselves from future financial disaster.

If you have some gaps, contact me. This is all covered by our planning process.