14 Questions to Ask a Financial Advisor Before Investing

It’s not easy finding a financial advisor. He or she needs to be someone you can trust with your hard earned money and you need to feel comfortable speaking candidly with them about your concerns, wants and needs. Asking these questions can help you decide out if this person is a good match for you and your family.

A Financial Advisor needs to be someone you can trust, you need speak candidly with them about your concerns, wants and needs. Asking these questions can help you decide if this person is a good match for you and your family.

Are you a fiduciary?

Yes. I am a fiduciary. From an SEC perspective, that means I list in my ADV form 2 how I get paid, the services I offer, and any conflicts of interest. Being a fiduciary means more than that to me: I put my clients interests ahead of my own. I work with trusted 3rd parties. I look for the best products for clients, taking into account quality, cost and timing. I don’t take any commission of any sort.

2. How do you get paid?

There are three ways I get paid:

Providing financial services on an ongoing basis. Monthly subscription of $125/month.

Creating a financial plan ($125/hour approximately 8-12 hrs).

1% of assets under management

For details on these offerings see Services.

3. What IS YOUR “all in” cost?

In addition to the services I outlined above, you would pay:

If I am managing your accounts, you would pay $15.95 per trade through my custodian, SSG.

Standard capital gains/losses on trades

.04%/year on ETFs (that comes to 40c per $1000/year)

4. What sort of tools do you use for budgeting?

I have a spreadsheet that utilizes a range of custom formulas that makes itemizing expenses, income and savings simple and easy to understand . Additionally, I have a variety of software and tools that facilitate the financial planning process.

5. How Do you deal with security?

My clients security is my top priority and is integral to my business. All of our assets are protected by multiple sets of encryption. Online access to accounts are protected. I use 2- factor authentication when sharing cleint information. Any spreadsheet/worksheet that I use is protected with unique and secure passwords.

6. What are your qualifications?

I work with families in a range life stages. I earned an undergraduate degree in Industrial Engineering from GA Tech and an MBA from Ga State. I passed the series 65 exam.

7. How would our relationship work?

I believe the key to a mutually beneficial long-term relationship is through trust and context. With that context I can better provide useful advice. I believe that meeting 1 time per year is not nearly enough. Our meeting cadence will be determined by my client’s situation as well as the issues needing addressed. My clients call, email and text me as needed and I respond in a timely manner.

8. What is your investment philosophy?

The best long-term results are achieved through creating an asset allocation that is well diversified, that will meet your goals (given your risk profile) and requires continual contributions.

I am not a stock picker. My solutions are data-driven. Historical data shows that the vast majority of stock pickers are not capable of beating their respective indexes, and generally end up with higher administrative fees.

I use low cost Exchange Traded Funds (ETFs). I believe the future will look better than the past, and as such, the best companies in the world, as represented by ETFs, will continue to appreciate over the long-term. I do not worry about the daily variations of the market, which tends to be irrational in the short term.

9. What benchmarks do you use?

The S&P 500 and inflation.

10. Who is your custodian?

A custodian is a company that performs trades and holds your shares. Eg: eTrade, Schwab, Fidelity. The custodian I use is Shareholders Service Group (SSG). They use Pershing a subsidiary of The Bank of New York Mellon, the largest custodian in the world with over $27 trillion in assets under custody.

11. What asset allocation will you use?

The majority of a client’s allocation should be in stocks rather than bonds and cash. Historical data shows that bonds barely keep up with inflation. The key to your future is in purchasing power, which means your money needs to beat inflation.

12. Give me an example of a portfolio you’ve designed AND ANY THOUGHTS ON HOUSING.

Each portfolio I design is specific to the client and their current financial situation, goals and risk attitude. As an example, one family I work with wants to reach their financial goals early. They contribute regularly and are mentally unaffected by the short-term variability of the market. At a high level their portfolio consists of low cost ETFs in an S&P 500 tracker: 30%, Emerging Markets: 30%, Small Caps: 30%, Cash: 10%.

Any thoughts on selling the family home now, and either renting or buying a less pricey house: this comes down to the goals of the family. While its true that many family’s biggest monthly expense, largest asset and largest liability is their home, it’s also true that it is their highest utilized asset. If you live in a house, that fits the size of your family, has attributes that you appreciate and does not cause you undue financial hardship … why mess up a good thing? If that set of “if’s” you cannot answer in the affirmative, and you can find a house that better meets your family goals … well it may make sense to move. As in stocks, I am not a believer in trying to time the housing market. I have heard rumors of friends in Decatur who are considering selling now (at a perceived high), renting for 2 years until a drop, and then buying again. I think thats crazy talk, for at least a dozen reasons.

13. What are the tax implications of working with you?

If I am managing your assets, any transaction sales will have some sort of tax implication, through capital gains/losses. I limit the tax implications by limiting the # of transactions.

14. WHY FAMILIES? WHY PROFESSIONALS?

In my experience the complexities of families deserve an added set of professional eyes administering a solid plan. There are many moving parts to a family, that include the expenses of starting a family, all the way into paying for college and eventually estate planning. More voices from a family generally brings more perspectives, something a trained professional can aid in clarifying.

Professionals are people driven to be really good at job, hopefully a job they love. In order to drive to be the best, many professionals are forced to neglect certain aspects of their lives. I have seen too many extremely smart professionals who have neglected their finances to the detriment of the long-term success of their family. I believe that by relieving families of this variable, we are all working for the greater good.

THE NEXT STEP

If you’re ready to take the next step toward financial independence, I’m here to help. Working together we will develop a personalized financial plan based on your unique needs. Set up an initial consultation.

Follow Us On Instagram: Chamberlain Financial

3 Hacks to Stay Motivated

The bigger the the goal, the longer it will take to reach. You’ve got to reward yourself along the way to stay motivated.

Planning for a long-term goal, while super important, feels remote for many people, check out my earlier post about meeting your future self. To stay motivated, I reward myself on a daily, monthly and yearly basis:

DAILY

A long-term health goal of mine is weighing in and maintaining a svelte 169 pounds. To get there I workout at Crossfit 2/week, play basketball and soccer 2/week, and practice intermittent fasting with an eating window between noon - 6pm. Meaning, I dont eat between the 6pm and noon the next day. Fasting helps me reach my weight goal, saves me lots of money and makes me realize I am tough enough not to constantly feed my urges. And it allows me to reward myself — when my eating window is open I treat myself to food I really like (thank you to the current ramen craze).

Monthly

One of my bedrock beliefs is “loving my friends and family.” It’s important to me that I have families come over to our house for Sunday Supper. I cook, the kids run around, and the adults mill about drinking wine, discussing football, the latest Netflix show and Decatur City Schools. For me, wine is a key element of Sunday Supper. I can’t deal with the uncertainty of randomly selecting bottles at the local wine shop. So each month, if I have met my business goals, I treat myself to 6 wines from Garagiste. Jon Rimmerman is the curator of Garagiste and he is all about value and honesty in wine making. I’m a big fan. With wine tucked away in the cellar, I am more likely to kick off the next Sunday Supper.

Yearly

Each month on payday, before we can spend it, we set aside a chunk of cash into a savings account for an awesome ski vacation and the kid’s sleep away camp. The ski trip gets us away from the daily grind, and allows us to team up against the mountain, working together and having a blast. Sending the boys away to summer camp serves two big goals for our family: 1. it teaches the boys independence and 2. it allows Jenn and I to connect and build on OUR relationship. We enjoy this without charging up a credit card by saving throughout the year.

Celebrate the baby steps

The bigger the the goal, the longer it will take to reach. You’ve got to reward yourself along the way to stay motivated. Enjoy life each day, but remember that the difference between a goal and a dream are the action steps you take.

Let’s talk about the hacks you use to keep yourself motivated through the year! A long-term plan is of minimal value, if you don’t have short-term games, that keep you motivated to play the long game. Schedule a quick chat today.

Big Bonus? Don't Ignore the Rainbow

from a sales/legal win). It always depends on your particular situation. However, there are some high level things I would suggest thinking about. First, have a plan!! I would go into it with split among your goals, Eg: 20% - short term, 60% - mid/long term, 20% - fun.

I have been asked for suggestions on what to do with a nice fat bonus check (or a big pay day from a sales/legal win). It always depends on your particular situation. However, there are some high level things I would suggest thinking about. First, have a plan!! I would go into it with split among your goals, Eg: 20% - short term, 60% - mid/long term, 20% - fun.

Short term issues that alleviate worry:

Pay down any high interest debt - credit card, 2nd mortgage, school loans

Put new tires on your car

Short/mid term value that you can add to your family

Time to upgrade your 10 year old minivan?

Remodel the kids bathroom?

Mid/long term investment for your future self

Fund an IRA

Fund an investment account

Buy into a real estate deal

Fund your safety cash (3 months of family bills)

Fund the kids 529’s

Do something for your self! It’s a bonus, enjoy it.

Buy yourself something fancy

Buy a gift for your sweet heart

Go for a ridiculously expensive dinner/outing

Check off an item on your bucket list

Hop on a plane for a far away spot for a week

Put a down payment on a Tesla

The key points here are:

Take care of some short term issues, that keep you up at night.

Think about your future self … they will be knocking on your door soon

HAVE SOME FUN

Warning: Don’t let your “bonus” fund your life.

If you are counting on your bonus to pay your bills, or keep you afloat for the year … please, pretty please with a cherry on top, you need to reevaluate how you are allocating your monthly income. Use this next bonus check, to catch you up. And lets go ahead and set up a plan, moving forward, so that you are focusing your spending on the things that matter to you. And not throwing money at things that don’t. Schedule a quick call or coffee!!

The Financial Mistake You Don't Realize You Are Making?

I was talking with a family friend, who’s retired, about how she was managing her affairs. She felt confident that all was well. She and her husband had recently updated their will. I nodded with approval,

I was talking with a family friend, who’s retired, about how she was managing her affairs. She felt confident that all was well. She and her husband had recently updated their will. I nodded with approval, as its always a wise move to have your will reevaluated every so often. I’m curious (nosy) and try to be helpful, so I asked her more questions. After I asked about her stock/bond/cash allocations, we moved on to insurance. I asked about long term care, in case circumstances changed and they needed assisted living. She got real quiet and then all of a sudden blew up in frustration …

“I didn’t think to ask about that but WHY DIDN’T THE LAWYER??!! I’m calling him tomorrow!”

It’s a common revelation to people I meet with: On your own, you’ve engaged with several specialists but don’t have a financial advisor with a holistic view of your entire financial health to make sure everything is covered. Similar to a primary care physician who sees you on a regular basis and advises when to see a trusted specialist. Or a systems architect in software, who understands how the myriad components of a system interact.

You may have someone for stocks and bonds, a medicare guru, an estate lawyer, a real estate lawyer and an insurance agent … but do you have anybody that has the overall holistic view of your plan, tying everything together? Someone who’s family’s future, is directly tied to your family’s future success?

At Chamberlain Financial Advisors, we assess all aspects of your situation, providing solid advice throughout. We are fee-only, meaning we don’t get commissions to sell you products. Where we need experts, I facilitate the conversation. The ultimate goal is your overall financial health.

Do you have an advocate with a holistic view of your family’s financial situation? Are you DIY’ing it, but don’t really understand all aspects of the plan? Set up some time with Josh. Let’s get fully healthy.

Why Would You Pay More For Xfit Each Month Than a Financial Advisor?

To stay healthy we pay ~$150/month for Crossfit or Yoga. Now you can have your own personal advisor working with you to ensure you meet your financial health goals, for less than your monthly health studio membership.

A recurring theme keeps coming up in conversations with potential clients... the idea that they "don't have enough dough" to "deserve" a financial advisor because they don't have significant investable assets lying around.

This notion, incidentally, is perpetuated by many advisors that won't talk to anyone with assets under $500,000! Because apparently their time/overhead is worth more than $5,000/client/year?

I became a financial advisor because of my love of investing and finance and my passion for helping others reach a place where cash is not the primary variable in determining a family’s long term decisions. It is important to me that my services are affordable and accessible so that I can build trustworthy and lasting relationships with as many people who could benefit from my help. To do all these things I have put together a win-win solution for those who don't have a boatload of assets -- yet.

Introducing Chamberlain Financial Advisors' Monthly Subscription

I want to work with people in their 30's and 40's that have great potential, realize they want to meet long term goals, and need someone they trust to help shepherd them through. I am offering a monthly subscription option, that is less than your monthly Crossfit or Yoga membership -- and it's equally as important for your (financial) health!

We will develop a regular cadence for meetings, virtual or in person, around your schedule. We will work on budgeting, investing, insurance (I’ve got a guy you can work with), saving for a house/boat/college expenses, annual company elections and anything else you may have on your mind. And as we work together, we will build a lasting relationship of trust.

Financial Planning & Investment Retainer

$125/month + $997 Upfront Fee

For those saving for retirement and who want to stay ahead of the game. Chamberlain Financial Advisors will create and manage your plan, guide your through the implementation process, monitor your investments and advise you as life changes.

Full implementation

Ongoing guidance

Investment advice

No asset requirement

Virtual planning available

Can you afford to put off this decision any longer? Do right by you and your family and start investing in your future. Schedule a call to discuss how, for less than your monthly cable bill, we can start building your wealth and reach financial freedom.

(**And Jenn and I love our fitness routines!! We love y’all @crossfitdecatur and @purebarredecatur.)

Why You Need to Friend Your Future Self

Think about you!

Yes, you. Where do you live? Who do you live with? Where do you work? How do you spend your free time? Now picture yourself in 10 years. Where do you live? Same place? Who do you live with? Are you working?... Do you have the same occupation?

Think about you!

Yes, you. Where do you live? Who do you live with? Where do you work? How do you spend your free time? Now picture yourself in 10 years. Where do you live? Same place? Who do you live with? Are you working?... Do you have the same occupation? How do you spend your free time?

In 2008, UCLA psychologist Hal Hershfield, Ph.D., conducted a study asking similar types of questions and found people commonly had two different neural patterns when thinking about the present versus the future: The first neural pattern: "I'm thinking about me". The second neural pattern: "I'm thinking about a stranger".

How you identify with your future self is called "self-continuity". Because many of us are not well connected to our future selves, we make decisions that maximize our current selves, and leave our future selves in bad shape. Check out this short article from Men's Health for more.

An example of this sort of behavior: On Friday watched the Atlanta United game with friends. As the game wound down, I ordered a parting drink. I certainly did not need it, and I had already scheduled an xfit workout the following morning. I failed to contemplate how my future self (only 8 hours into the future) was going to deal with waking up early and feeling crappy for my work out.

Get to know your future self and accomplishing your goals can be simpler than it seems.

Saving now, for either a short term goal such as a vacation, or a long term goal like retirement can seem vexing. And it will require a short term sacrifice. But your future self will appreciate it.

Here are a few things to get in touch with your future self:

1. Write a letter to your future self

2. Take a picture of yourself and run it through agingbooth or faceapp

3. Tap a surrogate, like your mom/dad, or someone with a similar job

4. Schedule a time with me and let me help get you connected

YOUR FUTURE SELF IS LOOKING FORWARD TO MEETING YOU!!

Lets schedule a quick 20 minute call to work on getting you to acquainted.

The END is NEAR!... Now What?

Fortune Magazine's August 2018 cover features a cryer with a placard reading "The END is NEAR". It discusses the longest US boom in stocks, is coming to an end. As evidence, it is using indicators that have sometimes (often?) been used in the past to determine a coming drop in the stock market:

Fortune Magazine's August 2018 cover features a cryer with a placard reading "The END is NEAR". It discusses the longest US boom in stocks, is coming to an end. As evidence, it is using indicators that have sometimes (often?) been used in the past to determine a coming drop in the stock market:

U.S. unemployment is nearing significant lows.

U.S. annual real GDP is dropping.

The treasury yield curve inversion is close (yield on short term exceeds the yield on long term treasuries.

The Federal deficit is ballooning.

Corporate debt is at all time high.

Oil has recently spiked.

Crucial Context: Wall Street analysts and industry pundits have never predicted both a drop and the timing of a drop.

So, what does this all mean? Mostly nothing.

The economy follows a standard pattern: expansion, peak, contraction and trough. Are we headed for a peak and contraction ... certainly. But that should not affect your investment patterns. Because an expansion will be just around the corner. And nobody has proven adept and timing the markets.

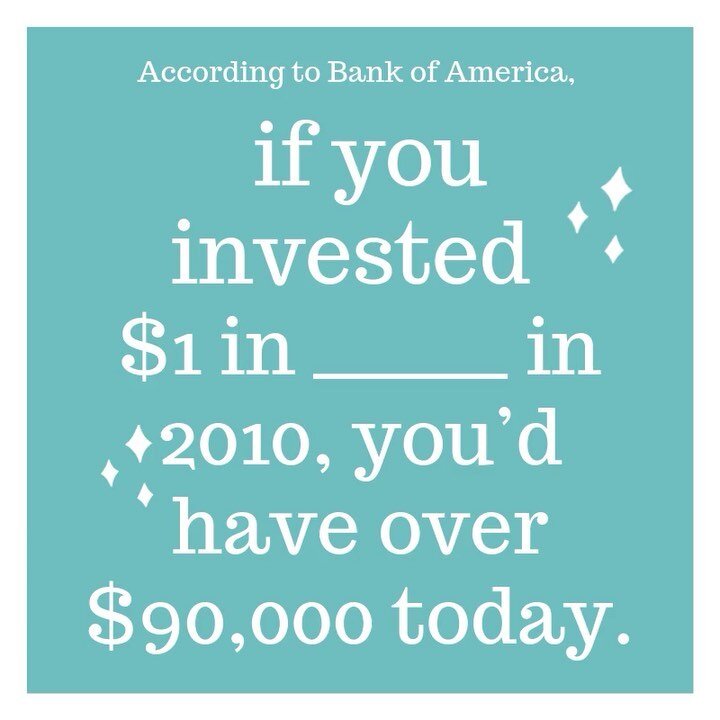

If you had sold at the top of the Oct 2007 and then waited for opportune buying times, you might have missed the 30 best days of the last 10 years. And if you had missed those 30 days? You would have realized a net loss of .9% ... as opposed to the 7.2% annual return, had you stuck it out and bought throughout that time.

So rest assured, a contraction is coming ...

...but don't worry, what follows will be an expansion. Continue to buy the best companies in the world at a discount throughout the process.

Are you mentally prepared for the coming drop?

Are you invested in a way that will cause you to run for the hills? Do you have an appropriate risk strategy that suits your style?

Let's talk if you need a second opinion on your portfolio.